Introduction

After a storm or sudden roof damage, homeowners often face the stress of filing an insurance claim. Once the insurance company sends an adjuster, you’ll receive an insurance estimate that lists the expected costs of repair or replacement. At this point, many people ask: Why does my roofer want to see this paperwork before giving me a quote?

The answer is simple but important. Roofing contractors need to compare your insurance paperwork with the actual scope of work on your home. This step protects you from hidden costs, delays, or even unintentional insurance fraud. In this guide from Relentless Roofing Co., we’ll explain why sharing your insurance estimate matters, what’s included in it, and how it affects your roofing project.

Why Do Roofing Contractors Ask to See the Insurance Estimate?

Roofing contractors ask for the insurance estimate so they can see what work has already been approved by your insurance company. Without this, the contractor may give you a completely different quote, leaving you to pay the difference out of pocket.

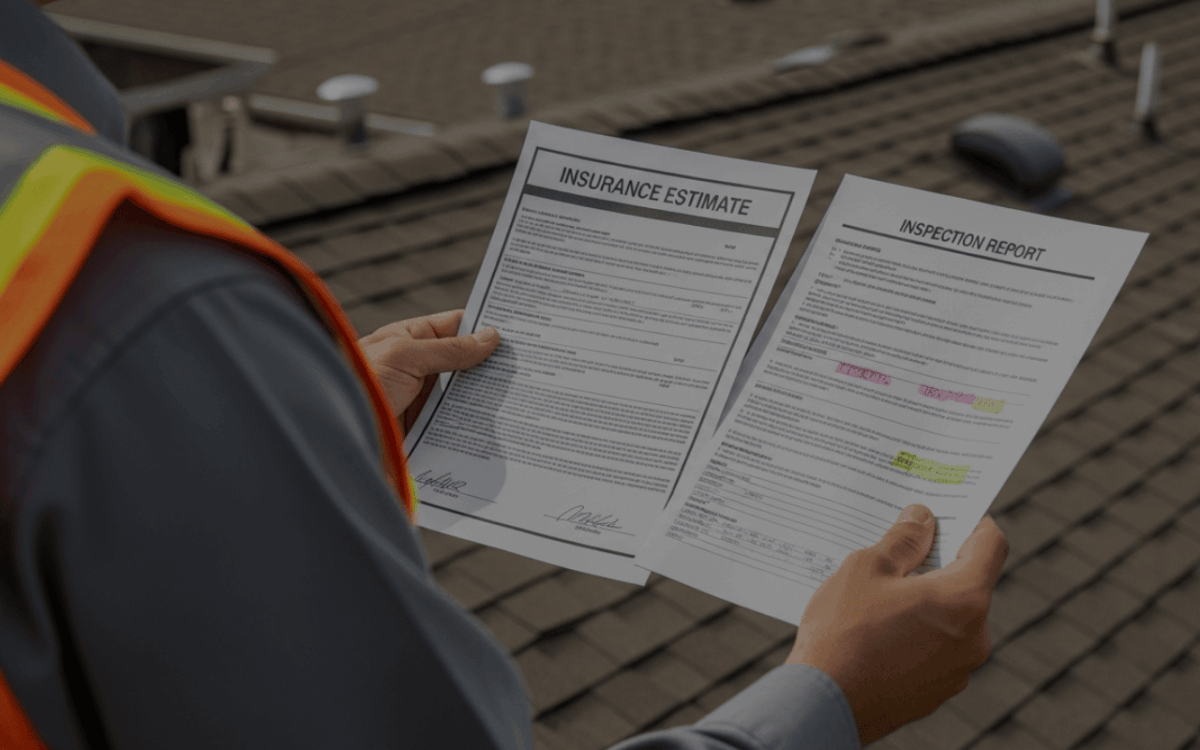

The insurance estimate shows the “scope of work,” which is the official list of repairs or replacements covered by your policy. By reviewing this, a roofer ensures their own estimate lines up with what the insurance company is willing to pay. This step also prevents mistakes, such as leaving off code-required upgrades or essential materials.

In short, roofing companies aren’t asking to see your paperwork to raise their prices. They’re asking so the job matches the insurance coverage you’ve already been granted.

What Is Included in a Roofing Insurance Estimate?

An insurance estimate is more than a simple price sheet. It’s a detailed document that lists:

- Labor costs for removal and installation

- Material costs such as shingles, flashing, and underlayment

- Permits and inspection fees required by your city or county

- Disposal and dump fees for removing old roofing

- Overhead and profit that contractors need to stay in business

It also includes a description of the roof damage, measurements, and sometimes photos taken by the adjuster. Homeowners should review this carefully with their roofing contractor to make sure nothing important is missing.

What Is a Supplemental Claim in Roofing?

A supplemental claim happens when the initial insurance estimate does not cover all the work needed. For example, an adjuster might leave out ventilation upgrades or miss damaged decking under the shingles.

When this happens, your roofing contractor can file a supplemental claim. They send documentation, photos, and proof of the extra items to the insurance company. Once approved, the insurer issues additional funds to cover those costs.

This process ensures you aren’t left paying for repairs that should have been included in the first place. It also helps bring your roof up to current building codes, which many adjusters overlook.

You may also read: The Ultimate Guide to Filing a Roofing Insurance Claim

Does Revealing Your Insurance Payout Lead to Higher Quotes?

Homeowners often worry that showing a roofer the insurance payout will encourage them to inflate prices. While this can happen with dishonest contractors, reputable roofing companies follow standard pricing guidelines used by insurance carriers.

In fact, sharing your paperwork protects you. If a roofer doesn’t know what your insurance company has already approved, they may give you a much higher estimate. That could force you to pay the gap out of pocket. By being transparent, you give the contractor a clear starting point and avoid surprises.

The key is choosing a certified, local roofer with a solid reputation. They will use the insurance estimate to make sure you get the repairs you’re entitled to—not to take advantage of you.

Why Is Reviewing the Insurance Estimate With a Contractor Important?

Reviewing your insurance paperwork with a contractor is essential for three reasons:

- Prevents Fraud – If the contractor doesn’t follow the insurance estimate, you could unknowingly commit fraud by requesting funds for incomplete work.

- Ensures Full Coverage – Contractors can spot missing items and request supplements to cover them.

- Builds Trust – By being open with your roofer, both sides work from the same information.

This review step gives homeowners peace of mind and helps the contractor plan the job correctly from day one.

You may also read: Insurance Says You Need a New Roof – Do You Really?

What Happens After the Insurance Adjuster Provides an Estimate?

Once the adjuster finalizes the insurance estimate, here’s what usually happens:

- The insurance company issues the first check (often based on Actual Cash Value).

- The homeowner shares the paperwork with a contractor for review.

- The contractor checks the scope of work, notes missing items, and may request supplements.

- Work begins on the roof.

- After completion, the contractor sends proof of work to the insurance company.

- The insurer releases the final payment (recoverable depreciation).

Having your roofer involved at this stage makes the process smoother and avoids delays in receiving the full payout.

ACV vs. RCV: What’s the Difference in Roofing Insurance?

Insurance policies usually fall under two categories:

- ACV (Actual Cash Value): Pays for the roof’s depreciated value. You’ll receive a smaller payout because it accounts for age and wear.

- RCV (Replacement Cost Value): Pays for a full roof replacement with new materials, minus your deductible. This is the most complete coverage option.

For homeowners, knowing the difference is crucial. An ACV policy often leaves you covering a bigger portion of the bill, while RCV provides more comprehensive protection.

| Feature | ACV (Actual Cash Value) | RCV (Replacement Cost Value) |

| How It Pays | Covers roof’s depreciated value (age + wear deducted) | Covers cost of a brand-new roof (minus deductible) |

| Payout Amount | Lower payout, often leaves homeowner paying extra | Higher payout, covers nearly all replacement costs |

| Homeowner Cost | You pay the difference between depreciated value and new roof cost | Only responsible for deductible + uncovered items |

| When It’s Used | Common in older policies or for older roofs | Preferred for full coverage and newer policies |

| Best For | Budget policies, homeowners with older roofs | Homeowners seeking full protection for roof damage |

How to Get a Fair Roof Estimate From a Contractor

Getting a fair estimate is about asking the right questions. Here’s how:

- Request 2–3 quotes from local, licensed roofers.

- Avoid contractors who promise to “waive your deductible.” That’s insurance fraud.

- Ask for itemized estimates that match the insurance paperwork.

- Check reviews and references before signing any agreement.

Fair pricing doesn’t mean the cheapest bid. It means the contractor’s estimate aligns with the scope of work approved by your insurance provider.

You may also read: Insurance Paid for a New Roof But It Looks Fine – What Should You Do?

Can Sharing Your Insurance Estimate Lead to Insurance Fraud?

Unfortunately, some scams involve insurance estimates. Shady contractors might offer to keep leftover funds, use inferior materials, or skip parts of the job. These practices put homeowners at risk of being accused of insurance fraud.

Legitimate roofing contractors will always match their work to the insurance paperwork. They’ll also provide a final invoice that reflects the exact scope of work. This protects you legally and financially.

Choosing the Best Roofing Contractor for an Insurance Claim Project

Finding the right roofer is more than just picking someone who can install shingles. When insurance is involved, you need a contractor who understands both roofing and the claim process.

Licensing and Insurance

Always confirm that your roofer is licensed and carries proper insurance coverage. This protects you from liability if accidents happen and ensures they meet state requirements.

Experience With Insurance Claims

Choose a contractor who regularly works with insurance claims and paperwork. They’ll know how to handle supplements, adjuster notes, and insurer communication from start to finish.

Local Reputation

Stick with a roofer who has a strong reputation in your community. Local contractors are easier to reach, trusted by neighbors, and less likely to vanish after the storm.

Clear Contracts

A trustworthy roofer provides written contracts with clear details on scope, pricing, and warranties. Avoid anyone offering vague promises or handshake agreements.

You may also read: Choosing the Right Roofing Contractor: 10 Key Questions to Ask

Conclusion

Showing your insurance estimate to a roofing contractor may feel risky, but it’s one of the smartest steps you can take after roof damage. It ensures the roofer knows the approved scope of work, protects you from unexpected costs, and helps avoid insurance fraud.

By working with a reputable, certified roofing contractor, you can trust that your roof repairs or replacement will be completed properly—and covered fairly by your insurance.

Key Takeaway

Sharing your insurance estimate with a roofing contractor is not about giving away leverage—it’s about protecting yourself. A roofer needs to see the paperwork to match the approved scope of work, request supplements if items are missing, and ensure your roof repair or replacement is fully covered. The right contractor won’t inflate prices but will guide you through the insurance process, keeping your project legal, fair, and stress-free.

FAQs

1. Should I share an insurance estimate with a contractor?

Yes, it helps the roofing contractor align their work with your insurance estimate and the approved scope of work from the insurance adjuster.

2. Do I need to tell the roofing company how much insurance gave me?

Yes, transparency prevents cost mismatches and protects the homeowner from issues like insurance fraud. Sharing your insurance paperwork lets the roofer know what line items are already covered.

3. What should I do if my contractor disagrees with my insurance estimate?

They can submit a supplemental claim with proof of missing line items, roof repair needs, or code upgrades. This ensures the insurance company covers all necessary work.

4. Can my contractor help me negotiate with my insurance company?

Yes, experienced roofing companies often communicate directly with insurance adjusters. A roofer familiar with the claim process can make sure nothing is overlooked in your insurance policy coverage.

5. Does homeowners insurance cover a full roof replacement?

It depends on the cause of roof damage, your insurance policy type (ACV vs. RCV), and the adjuster’s findings. In many cases, an insurance claim will cover roof replacement if the damage is storm-related.